What is meant by swap example with example?

The definition of a swap is a trade or exchange. An example of a swap is a child trading his pretzels for popcorn at snack time. noun. 1. To trade one thing for another.

How do you explain interest rate swaps?

Interest rate swaps are forward contracts where one stream of future interest payments is exchanged for another based on a specified principal amount. Interest rate swaps can exchange fixed or floating rates in order to reduce or increase exposure to fluctuations in interest rates.

What is the most common type of interest rate swap?

The most commonly traded and most liquid interest rate swaps are known as “vanilla” swaps, which exchange fixed-rate payments for floating-rate payments based on LIBOR (London Inter-Bank Offered Rate), which is the interest rate high-credit quality banks charge one another for short-term financing.

What do swap rates tell us?

Swap rate denotes the fixed rate that a party to a swap contract requests in exchange for the obligation to pay a short-term rate, such as the Labor or Federal Funds rate. Swaps are typically quoted in a swap spread, which calculates the difference between the swap rate and counter-party rate.

What are types of swap?

- Interest Rate Swaps.

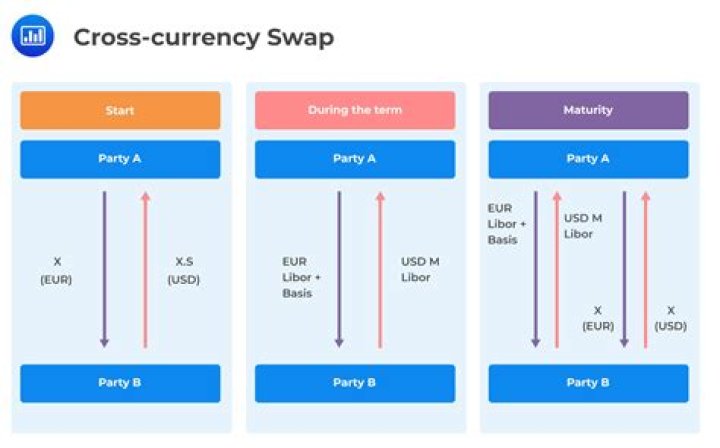

- Currency Swaps.

- Commodity Swaps.

- Credit Default Swaps.

- Zero Coupon Swaps.

- Total Return Swaps.

- The Bottom Line.

How does a FRA work?

Forward rate agreements (FRA) are over-the-counter contracts between parties that determine the rate of interest to be paid on an agreed-upon date in the future. The notional amount is not exchanged, but rather a cash amount based on the rate differentials and the notional value of the contract.

How many main types of swaps are there?

The generic types of swaps, in order of their quantitative importance, are: interest rate swaps, basis swaps, currency swaps, inflation swaps, credit default swaps, commodity swaps and equity swaps. There are also many other types of swaps.

What is the difference between interest rate swap and forward rate agreement?

Effectively, an FRA is a short-term, single-period interest rate swap. Only interest flows are exchanged and no principal is exchanged. In a generic FRA one party pays fixed and the other party pays floating. The settlement reflects the difference between the FRA rate and the floating rate set for the period.

What is an example of an interest rate swap?

How Interest Rate Swaps Work Generally, the two parties in an interest rate swap are trading a fixed-rate and variable-interest rate. For example, one company may have a bond that pays the London Interbank Offered Rate (LIBOR), while the other party holds a bond that provides a fixed payment of 5%.

What is an example of a float to fixed swap?

A floating-to-fixed swap is where a company wishes to receive a fixed rate to hedge interest rate exposure, for example. Lastly, a float-to-float swap—also known as a basis swap—is where two parties agree to exchange variable interest rates. For example, a LIBOR rate may be swapped for a T-Bill rate.

What is a basis swap?

A basis swap is a variation of the standard interest rate swap with the particularity that the two interest rate flows which are exchanged are both variable rates, indexed on two different interest rate indexes. An example would be a 3-month LIBOR against a 6-month LIBOR.

What is the difference between variable rate and amortizing swap?

A variable interest rate is a rate on a loan or security that fluctuates over time because it is based on an underlying benchmark interest rate or index. An amortizing swap is an interest rate swap where the notional principal amount is reduced at the underlying fixed and floating rates.