Can Heteroskedasticity causes OLS estimator to be biased?

Heteroskedasticity does not cause ordinary least squares coefficient estimates to be biased, although it can cause ordinary least squares estimates of the variance (and, thus, standard errors) of the coefficients to be biased, possibly above or below the true or population variance.

Does Heteroskedasticity affect bias?

While heteroskedasticity does not cause bias in the coefficient estimates, it does make them less precise; lower precision increases the likelihood that the coefficient estimates are further from the correct population value.

Is OLS consistent with Heteroskedasticity?

Heteroskedasticity has serious consequences for the OLS estimator. Although the OLS estimator remains unbiased, the estimated SE is wrong. Because of this, confidence intervals and hypotheses tests cannot be relied on. In addition, the OLS estimator is no longer BLUE.

Which statistics are biased in the presence of heteroscedasticity?

Heteroscedasticity does not cause ordinary least squares coefficient estimates to be biased, although it can cause ordinary least squares estimates of the variance (and, thus, standard errors) of the coefficients to be biased, possibly above or below the true of population variance.

What are heteroskedasticity robust standard errors?

“Robust” standard errors is a technique to obtain unbiased standard errors of OLS coefficients under heteroscedasticity. Remember, the presence of heteroscedasticity violates the Gauss Markov assumptions that are necessary to render OLS the best linear unbiased estimator (BLUE).

How does heteroscedasticity impact model estimates?

While heteroscedasticity does not cause bias in the coefficient estimates, it does make them less precise. Lower precision increases the likelihood that the coefficient estimates are further from the correct population value. Heteroscedasticity tends to produce p-values that are smaller than they should be.

How does heteroskedasticity affect standard errors?

Does heteroskedasticity increase standard error?

Only if there is heteroskedasticity will the “normal” standard error be inappropriate, which means that the White Standard Error is appropriate with or without heteroskedasticity, that is, even when your model is homoskedastic.

What problem does heteroskedasticity cause for the OLS estimators show mathematically?

A nonconstant error variance, heteroscedasticity, causes the OLS estimates to be inefficient, and the usual OLS covariance matrix, ∑, is generally invalid: (6.22) for some, j > 1.

Why is heteroskedasticity a problem?

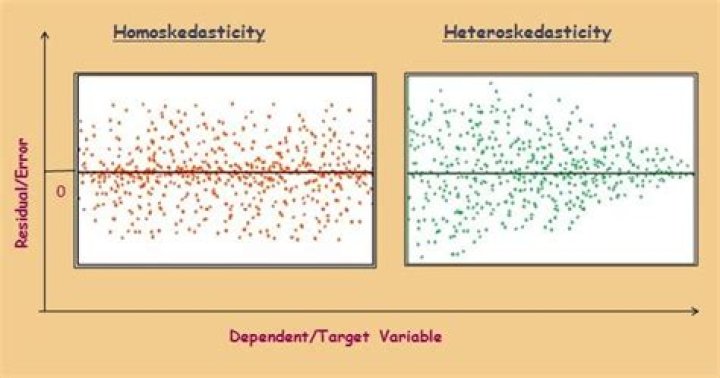

Heteroscedasticity is a problem because ordinary least squares (OLS) regression assumes that all residuals are drawn from a population that has a constant variance (homoscedasticity). To satisfy the regression assumptions and be able to trust the results, the residuals should have a constant variance.

What does robust standard error do?

Robust standard errors, also known as Huber–White standard errors,3,4 essentially adjust the model-based standard errors using the empirical variability of the model residuals that are the difference between observed outcome and the outcome predicted by the statistical model.

What are the problems of econometrics?

Typical Problems Estimating Econometric Models

| Problem | Definition |

|---|---|

| High multicollinearity | Two or more independent variables in a regression model exhibit a close linear relationship. |

| Heteroskedasticity | The variance of the error term changes in response to a change in the value of the independent variables. |